S&P and Consumer Sentiment in Sharp Decline as Volatility Persists

Market Summary

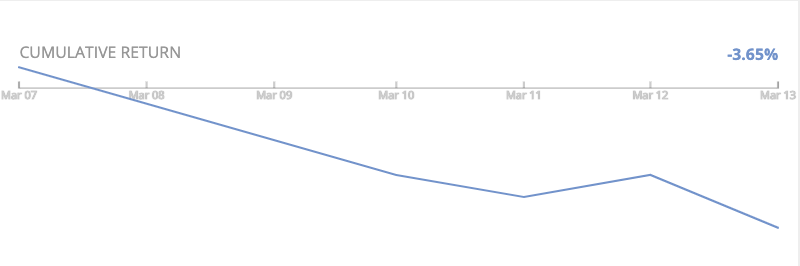

US Market: 3/07/2025 - 3/13/2025

- U.S. headline indices continued their recent decline as the S&P 500 was down -8.29%, the NASDAQ fell -4.03%, and the Dow Jones declined -3.98%.

- The S&P 500’s current correction has seen the index lose over 10% in only 16 trading days since it’s all-time high on February 19th. This drawdown occurs as the scope of expected retaliatory tariffs and federal layoffs has increased.

- US consumer sentiment, as measured by the University of Michigan survey, dropped to 57.9, the lowest level since November 2022. Inflation expectations jumped by the most since 1993, with consumers expecting prices to rise 4.9% over the next year.

- The price of gold surpassed $3,000 an ounce for the first time ever. The price increase has come as a result of investors seeking safer assets and central banks buying bullion to diversify away from the dollar. Gold prices have risen 10x in the last 25 years, outperforming the S&P 500, which increased four-fold over the same period.

Extreme Movers Portfolio Performance

Note: Extreme Movers definitions can be found in the Factor University section on our website.

US Extreme Moves Volatility and Factor-Driven Speedometers

- The US Extreme Movers portfolio saw a 17.6% return this week, ranking in the 71st percentile for the trailing twelve months and the 80th percentile since inception. This level of performance marks the week as being “Volatile”.

- Factors accounted for 29.9% of the total return, placing the portfolio in the “Factor-Driven” category. This ranks in the 78th percentile for the trailing twelve months and the 70th percentile since inception.

International Extreme Movers Volatility and Factor-Driven Speedometers

- The International Extreme Movers portfolio earned a 17.7% return, placing it in the "Volatile" category for the week. This return ranks in the 86th percentile over the trailing twelve months and the 77th since inception.

- Factors accounted for 25.8% of the total return, which classifies as "Neutral". This level of factor return is in the 47th percentile for the portfolio over the trailing twelve months and the 44th since inception.

US Extreme Movers Portfolio Exposures

- This week, the energy sector saw a big jump, becoming the largest sector in the US extreme movers portfolio with a 19% allocation. This is a pretty significant weighting, putting the sector in the 97th percentile over the past year and the 88th percentile since the portfolio started. Within the energy sector, the Oil, Gas & Consumable Fuels industry took the top spot, making up 18% of the total allocation.

- Consumer Staples secured the second-largest allocation in the portfolio with 11%, ranking in the 92nd percentile for the past twelve months and the 94th percentile since the portfolio's inception. All sectors within the sector played a part in this strong allocation, with Food Products being the biggest contributor at 5%

- Consumer Staples remained the least represented sector this week, with a -21% allocation. This placed the sector in the 11th percentile over the past twelve months and the 6th percentile since the portfolio’s inception. The majority of this short allocation came from the Hotels, Restaurants & Leisure industry, which made up -15% of the total short allocation by itself.

- This week, Value factors were strongly favored, with all factors landing above the 90th percentile for the trailing twelve months. Notably, Wolfe's Dividend Yield ranked at the top for both the trailing twelve months and since the portfolio's inception. Both the long and short books of the portfolio contributed equally to this exposure, suggesting that investors were shorting stocks with low dividend yield and going long on those with high dividend yield.

- Crowding factors were mixed this week. HF Crowding saw its lowest exposure since the portfolio’s inception, with a -1.28 exposure. This negative exposure came entirely from the short side, particularly in the Software and Hotels, Restaurants, and Leisure industries. On the flip side, ETF Flow performed well, ranking in the 95th percentile for the trailing twelve months and the 88th percentile since inception. The main contributors to this were short positions in the Information Technology and Consumer Discretionary sectors.

- Growth factors were out of favor this week, with both the Axioma and Barra growth factors landing in the bottom decile of the data. Both the long and short sides of the portfolio contributed equally to this allocation

International Extreme Movers Portfolio Exposures

- The Materials sector secures its position as the most represented this week, with a 13% allocation. This places the sector in the 90th percentile for the trailing twelve months and the 85th percentile since the portfolio's inception. Within this sector, Metals and Mining stands out as the leading industry, making up approximately 8% of the total allocation on its own.

- The Energy sector ranked as the second most represented this week, with an 8% allocation. This places the sector in the 98th percentile for the trailing twelve months and the 85th percentile since the portfolio's inception. All of this exposure is derived from the long book of the portfolio, primarily within the Oil, Gas & Consumable Fuels industry.

- Finally, Information Technology remained the least represented sector, with its allocation shifting from -21% last week to -13% this week. This allocation places the sector in the 9th percentile for the trailing twelve months and the 5th percentile since the portfolio's inception. The negative allocation was driven by all industries within the sector, except for Communications Equipment.

- Value factors were favorable this week for the International Portfolio, with all factors landing above the 90th percentile for both inception-to-date and trailing twelve-month periods. Barra's Dividend Yield factor saw particularly high exposure at 0.68, the highest for the trailing twelve months. The majority of this exposure came from the short book of the portfolio, with the long book contributing as well, though to a lesser extent.

- Macro factors also worked in favor, particularly the Oil Beta factor, which landed in the 95th percentile for the trailing twelve months. Most of this exposure came from the long book of the portfolio. Interest rate beta was also favorable, though to a lesser extent.

- In contrast, growth factors were out of favor this week. Axioma’s growth factor landed in the 5th percentile for the trailing twelve months and the 19th percentile since the portfolio's inception. The long allocation to Industrials and the short allocation to the Healthcare sector were the primary contributors to this negative exposure.

International Extreme Movers Portfolio Country Exposures

This chart presents the portfolio's exposures to various groups in the Developed and Emerging Markets, highlighting the three most notable country contributors for each respective group's allocation.

- After several weeks, Emerging Markets were back in favor this week with a 13% allocation, placing the region in the 13th percentile for both the trailing twelve months and since the portfolio's inception. In contrast, Developed Markets saw a -12% allocation this week, which placed the region in the 23rd percentile for the trailing twelve months and the 26th percentile since the portfolio's inception.

- Within Emerging Markets, The Americas had the highest allocation at 6%, with Brazil being the largest contributor, accounting for 5% on its own. While Asia contributed the least to the EM allocation, China was well represented with a 22% exposure. However, other countries in the region had short allocations, which netted Asia's overall contribution down to 3%.

- For Developed Markets, Europe & the Middle East had the smallest allocation at -6%, with the UK being the primary driver, contributing -5% on its own. This placed the UK in the 2nd percentile for the trailing twelve-month period. The Pacific region also saw a -6% allocation, with Australia having the largest impact, contributing -5% by itself.

Regards,

Colin

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

Join us this week as we analyze a US market rebound and other significant macroeconomic events impacting global markets.

Central bank decisions and economic data shake global markets: Explore how the Bank of Japan's surprise announcement and US job market report impacted currencies, stocks, and investment strategies. Gain insights on factor performance and market reactions to help inform your portfolio decisions.

This week we explore the market’s leap into interest-rate-correlated stocks following hot European inflation reports and spiking bond yields.