Trump Tariffs Unleash Market Turmoil

Market Summary

US Market: 3/28/2025 - 4/3/2025

- President Donald Trump announced Wednesday that all nations would be subject to at least a 10% tariff going forward, with higher “reciprocal“ rates for countries deemed to have high barriers on US goods. This led to a significant market rout, with the Dow Jones Index tumbling 1679 points on Thursday, the S&P down 4.84%, and the Nasdaq sliding 6%.

- China struck back with it’s own tariff announcements Friday, imposing a slew of levies including an additional 34% on all US goods starting April 10th, on top of previous tariffs imposed in February and March. As the third largest buyer of US goods, the additional tariffs are expected to heavily impact Chinese imports, opening up opportunity for other exporters like Brazil and Australia to capture more market share.

- US Jobs data released Friday showed unexpectedly strong jobs growth in March, with 228,000 jobs added despite the unemployment rate rising to 4.2%. The report suggested steady momentum in the economy prior to this week’s tariff announcements that sparked global retaliation threats. Many analysts now expect that the resilience indicated by the report is no longer a good indication of what’s to come.

Extreme Movers Portfolio Performance

Note: Extreme Movers definitions can be found in the Factor University section on our website.

US Extreme Moves Volatility and Factor-Driven Speedometers

- The US Extreme Movers portfolio saw a 14.5% return this week, ranking in the 43rd percentile for the trailing twelve months (TTM) and the 63rd percentile since inception. This level of performance marks the week as being “Volatile”. The divergence in the TTM and since-inception percentiles indicates the elevated levels of volatility the market has seen in the past year.

- Factors accounted for 28.4% of the total return, placing the portfolio in the “Factor-Driven” category. This ranks in the 78th percentile for the trailing twelve months and the 65th percentile since inception. Industry factors drove two thirds of the total factor return.

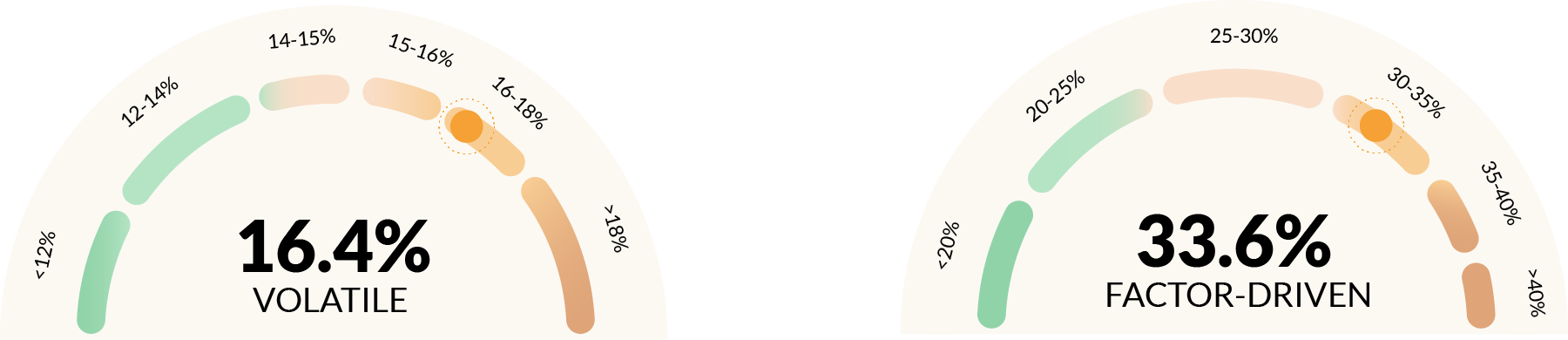

International Extreme Movers Volatility and Factor-Driven Speedometers

- The International Extreme Movers portfolio earned a 16.4% return, placing it in the "Volatile" category as well for the week. This return ranks in the 63rd percentile over the trailing twelve months and the 67th since inception.

- Factors accounted for 33.6% of the total return, which classifies as “Factor-Driven". This level of factor return is in the 80th percentile for the portfolio over the trailing twelve months and the 75th since inception. Country and Industry factors drove almost 80% of the total factor return.

US Extreme Movers Portfolio Exposures

- The Consumer Staples sector was the largest sector in the US extreme movers portfolio with a 24% allocation this week. This was the sector’s highest ever allocation since the portfolio’s inception. Within the sector, the Consumer Staples Distribution & Retail industry accounted for 10% of the portfolio.

- Utilities was the second largest allocation in the portfolio at 13%, ranking in the 98th percentile for the past twelve months and the 96th percentile since the portfolio's inception. Electric Utilities was the biggest Industry contributor at 9%.

- Information Technology was the least represented sector this week, registering a -37% allocation. This placed the sector in the 2nd percentile over the past twelve months and since the portfolio’s inception. The majority of this short allocation came from the Software industry, which made up -15% of the portfolio.

- Value Factors were in favor this week across all models. The Dividend Yield exposure was driven by the short book, and the portfolio’s short Tech position specifically. Earnings Yield was also driven by the short book, in particular the Health Care and Tech sectors. US investors were looking to sell names with low beta to Value in these sectors.

- Beta and Volatility factors were out of favor this week as all but Axioma’s volatility were in the red this past week. This negative exposure was driven by the short book, and predominantly the Tech short, as investors unloaded high vol names in the sector.

- Quality factors provided further evidence of the current risk-off environment in US markets, as all factors in the category were strongly in favor this week. Profitability was especially in favor as exposure to the factor placed in the top decile for the trailing twelve months and since inception for the Axioma and Wolfe models. The exposure for each came from the Tech and Health Care shorts in the portfolio.

International Extreme Movers Portfolio Exposures

- The Utilities sector was the most represented sector in the International portfolio this week, with a 15% allocation. This is the sector’s highest allocation over the last year and is in the 99th percentile since the portfolio's inception. Electric Utilities was the leading industry, making up 5.9% of the portfolio allocation.

- Consumer Staples ranked as the second most represented this week, with a 13% allocation. This allocation was also the highest for the sector over the trailing twelve months and in the 97th percentile since the portfolio's inception. This exposure was driven primarily by Consumer Staples Distribution & Retail at 5.3%.

- Information Technology was the least represented sector in the International portfolio as well, its allocation was -25% this week. This is the lowest allocation for the sector since the portfolio's inception. Semiconductors & Semiconductor Equipment drove most of the negative exposure for the sector at -13%.

- Beta and Volatility factors were out of favor this week in the international portfolio. Barra’s Beta factor stood out, as it registered its lowest exposure in the portfolio over the past year, this was driven by the portfolio’s long holdings. The negative exposure for the remaining factors in the category was driven by the short Tech and Industrials positions.

- There was dispersion amongst the two models in the Growth category this week. Axioma’s Growth factor was in favor and was driven by the portfolio’s short book, specifically Consumer Discretionary and Materials. Barra’s Growth factor was heavily out of favor, in the bottom decile for TTM and ITD, and was also driven the by the short book, in particular Tech names.

- Macro factors were heavily out of favor this week. Wolfe’s Oil Beta factor placed in the 8th percentile over the past year and their Interest Rate Beta factor placed in just the second over the same period. The portfolio’s short materials position was the primary driver of the low exposure for each factor.

International Extreme Movers Portfolio Country Exposures

This chart presents the portfolio's exposures to various groups in the Developed and Emerging Markets, highlighting the three most notable country contributors for each respective group's allocation.

- Emerging Markets were in favor this week with a 5% allocation, placing the region in the 59th percentile for the trailing twelve months and the 54th since the portfolio's inception. Developed Markets saw a -5% allocation this week, which placed the region in the 30th percentile for the trailing twelve months and the 37th percentile since the portfolio's inception.

- Within Emerging Markets, the Americas had the highest allocation at 7%, with Mexico the largest contributor at 3%.

- For Developed Markets, the Pacific region had the lowest allocation at -16%. This was mainly due to Japan, which had a -19% allocation.

Regards,

Colin

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week we unpack the latest rout of market volatility, incited by trade frictions, waning risk sentiment, and monetary policy decisions.

Join us as we explore another volatile week in US markets with investors rushing to make sense of an economic slowdown, geopolitical uncertainty, and an escalating trade war.

This week, we explore turbulent market conditions as the Fed reiterates its “higher for longer” rate policy, bond yields skyrocket, and geopolitical tensions escalate.